Bangladesh’s FY2026-27 budget promises to wean the economy off bank borrowing. The pivot is real as a ratio — but it is mostly an accounting effect, and the deeper problem it skirts is revenue.

Image: AI Generated

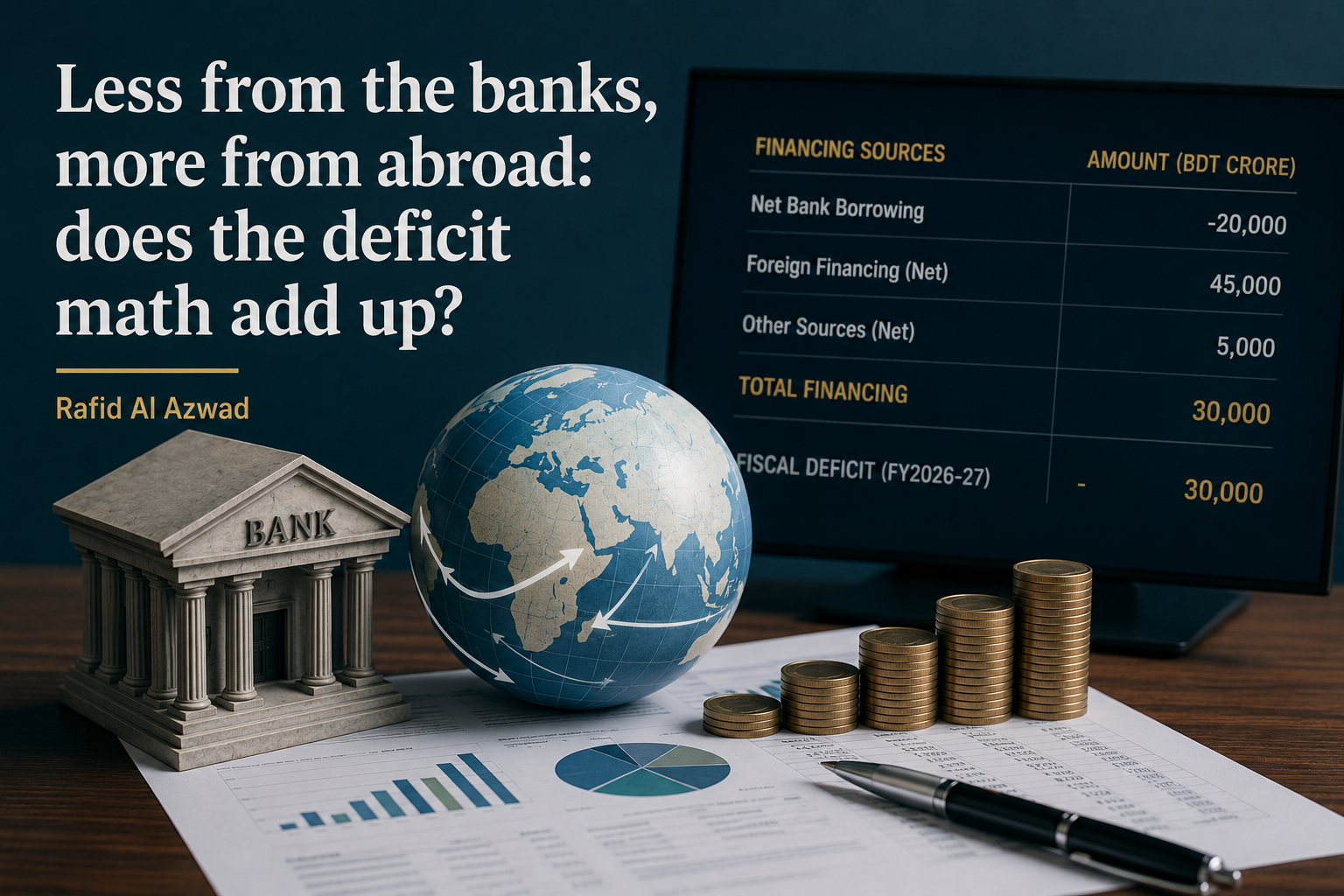

Every June, Bangladesh unveils a budget bigger than the last, and every June the more revealing number is not what the government plans to spend but how it plans to pay for what it cannot cover. For FY2026-27 — the first budget of the newly elected BNP government — the headline is a record outlay of Tk 9.38 trillion and a deficit of roughly Tk 2,43,000 crore, about 3.6 percent of GDP. The deficit itself is unremarkable by international standards, sitting comfortably below the informal five-percent ceiling. The real story is in the financing plan, and in a single claim the government has placed at its centre: that it will reduce the economy’s dependence on bank borrowing and lean instead on foreign financing, freeing up resources for private investment and easing inflation.

It is a tidy narrative. It is also worth examining slowly, because the most prominent piece of evidence offered for it — the one printed in the government’s own Citizen’s Budget — proves less than it appears.

That graphic tells citizens that financing from the banking sector will fall from 59 percent of total deficit financing in the revised FY2025-26 budget to 46 percent in FY2026-27. A thirteen-point drop sounds like a decisive turn away from the banks. However, let us look at the underlying taka figures. Bank borrowing falls from about Tk 1,18,000 crore to Tk 1,12,000 crore — a cut of barely five percent. The share collapses so much further only because the denominator beneath it swelled: the total deficit grew by more than a fifth, and that growth was financed almost entirely by a near-doubling of net foreign borrowing, which jumps roughly 89 percent to about Tk 1,10,000 crore. The government, in short, is not so much borrowing less from banks as borrowing far more from abroad — which makes the bank slice look smaller by comparison. The reduced dependence is real as a ratio, but it is largely a denominator effect, not a genuine retreat from the domestic banking system.

Why does the distinction matter? Because the entire economic case for the strategy rests on the idea that bank borrowing was crowding out private investment — that the government, by stepping back, will leave more credit for businesses and push interest rates down. The trouble is that this logic, intuitive as it sounds, does not fit Bangladesh’s present circumstances, and the local evidence behind it has never been settled.

Consider the research. A Bangladesh Bank working paper by Majumder (2007) found no crowding-out of private investment from public borrowing; a study by the Bangladesh Institute of Development Studies went further, concluding that public investment financed by borrowing actually encouraged private investment by building the infrastructure firms need. Other studies, using different methods and periods, do detect a crowding-out effect. The honest summary is that the question is genuinely contested — which means neither the government nor its critics should claim the answer with confidence.

More tellingly, the banking system today is not short of money. Banks are holding excess liquidity reported at around 55 percent, and the loan-to-deposit ratio has slipped as private credit demand stays weak. If firms are not borrowing, it is not because the government has crowded them out of a scarce pool of funds; it is because investment confidence is low, energy and policy uncertainty is high, and the banks themselves are ailing. Non-performing loans peaked at nearly 36 percent of all loans last year — briefly the highest ratio in the world — and the sector’s capital adequacy turned negative for the first time in the country’s history. Against that backdrop, trimming government bank borrowing by five percent is unlikely to unleash a wave of private investment. The binding constraint lies elsewhere.

If the domestic story is oversold, the foreign-financing pivot deserves a fairer hearing. Borrowing abroad has real advantages: concessional loans from the World Bank and the Asian Development Bank carry longer maturities and lower rates than domestic debt, they bring in foreign exchange to shore up reserves, and anchoring the budget to an IMF reform programme signals discipline to investors and rating agencies. But the pivot carries risks that the friendly net figures understate. The Citizen’s Budget shows external financing of Tk 1,16,000 crore; it does not show that gross foreign borrowing is far larger — on the order of Tk 1.55 trillion — with a sizeable share merely servicing old loans. Nor can a graphic resolve the two hard questions. The first is the taka: foreign-currency debt grows more expensive in local-currency terms every time the currency weakens, as it has, and the cheapness of external borrowing can evaporate through the exchange rate — as Sri Lanka learned in 2022. The second is absorption: project loans flow only as fast as projects are built, and Bangladesh’s development-budget implementation recently fell to around 20 percent, the lowest in fifteen years. Securing the money is one thing; spending it well is another.

The academic record counsels caution here too. Most Bangladesh-specific studies — Shah and Pervin (2012), Milon and colleagues (2024) — find that external debt has, on balance, weighed on growth rather than lifted it, while a more hopeful strand argues the drag can be offset by sound macroeconomic management. The lesson is not that foreign borrowing is a trap, but that it is a wager whose payoff depends on a stable currency, productive use, and rising revenue to service it later.

To add, revenue is where this whole conversation should arguably begin. Every financing dilemma in the budget is downstream of one stubborn fact: Bangladesh collects less tax, relative to the size of its economy, than almost any country in Asia. Its tax-to-GDP ratio — somewhere between 7 and 8 percent — is less than half the 15 percent generally treated as the minimum for a functioning state, and it has been stuck below 10 percent for half a century despite repeated pledges and donor help. The revenue target written into this budget would require collection growth the country has never achieved; last year ended in a record shortfall. A state that cannot collect its own taxes must borrow simply to run itself — and then argue, as we are arguing now, over whether to borrow from banks or from abroad. That argument is a symptom. The disease is the revenue base, hollowed out further by tax exemptions that forgo revenue worth several percent of GDP. Until that base is broadened and the exemptions rationalised, no rearrangement of the financing mix will make the arithmetic sustainable.

To its credit, the budget gestures at a more durable answer, promising to develop the bond market and issue corporate and municipal bonds to fund long-term investment from non-bank sources. The ambition is sound. Nevertheless, Bangladesh’s corporate bond market is thin and a municipal bond market scarcely exists; this is a project for years, not a financing line for the coming one.

It is fair to read the budget as a political document, because that is partly what it is. The Citizen’s Budget plots the deficit-to-GDP ratio across three carefully chosen years — 2.90 percent in 2005-06, 4.05 percent in 2023-24, and 3.60 percent now — an arc of discipline, then expansion, then discipline restored. The selected anchors happen to be the last previous BNP government, a peak Awami League year, and the new BNP government. The comparison is accurate and curated at once, and a reader is entitled to notice both. An administration elected after an uprising in which inflation and joblessness were central grievances has every reason to present a budget that foregrounds stability and the private sector. None of that makes the economics wrong; it means the plan should be judged on delivery rather than on its framing.

So, does the deficit math add up? On paper, yes — the numbers balance, the deficit is modest, the strategy is internally coherent. In practice, it leans on two assumptions that have seldom held together in Bangladesh: that revenue will climb steeply, and that foreign funds will be absorbed quickly. If either one slips — and history suggests at least one will — the government will do what governments here have always done when the money runs short, and turn back to the banks. The modest planned cut in bank borrowing is the first thing likely to be reversed mid-year. That is the quiet vulnerability beneath the confident graphics. The verdict is not that the plan is reckless, but that its headline achievement — weaning the economy off bank borrowing — is smaller than advertised, and its success hinges on the one thing a single budget cannot fix: how little this state collects from those it governs. The rest, for now, is arithmetic.

About Author:

Rafid Al Azwad

Executive, TBD